Simple bank offers no fees and budgeting tools—but is it right for you?

Everything you need to know, from joint accounts to automatic savings goals

Credit:

Getty Images / RyanJLane

Credit:

Getty Images / RyanJLane

Recommendations are independently chosen by Reviewed's editors. Purchases made through the links below may earn us and our publishing partners a commission.

Maybe you’ve seen advertising for Simple that has left you wondering what exactly it is. In short, the company offers fee-free checking, savings, and certificate of deposit accounts with simple terms—hence the name.

This may all sound like the trappings of a bank, but Simple isn’t actually a bank at all.

While you manage your money through Simple, funds you deposit are held by BBVA USA, its FDIC-insured bank partner.

And unlike traditional bank accounts, Simple’s online accounts don’t come with the terms or conditions that are typical of brick-and-mortar financial institutions.

This all sounds pretty great. But are you willing to hand over your cash knowing that you can't walk into a branch if something goes wrong? Here’s what you can expect.

What are Simple's online banking terms?

These terms are subject to change—and they've changed a bit even over the time we conducted this review—but as of publication, here are the rates, fees, and other terms you'll get with a Simple account:

- Minimum balance required to open: None

- Monthly fee: None

- Overdraft fee: None

- ATM fees: None with Allpoint® ATMs, though you won't be reimbursed for fees incurred outside of the network

- Foreign transaction fee: Up to 1% charged by Visa

- Online checking APY: 0.00%

- High-yield savings APY: 0.60%

- Certificate of deposit APY: 0.50%

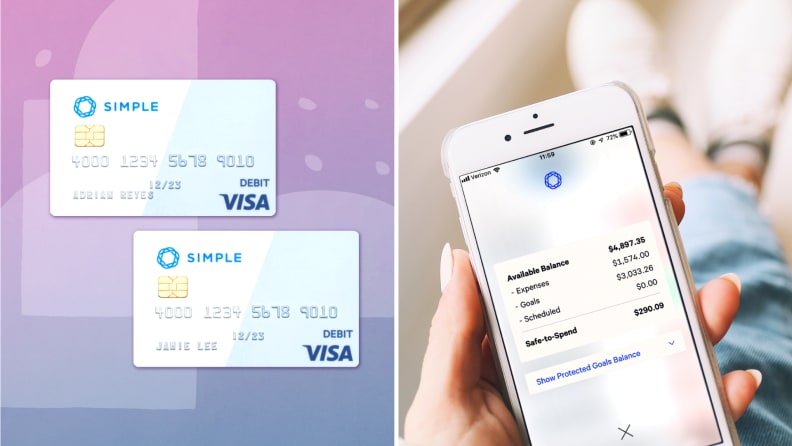

Couples may find Simple's joint accounts useful when merging finances.

Who should consider using Simple?

Simple is not just a bank account—it’s also an app that helps you oversee your finances with a sleek user interface and money management tools. If you’re someone who’s looking for a bank account and a budgeting solution, this could be a good choice. But you need to be at least 18 years old with a Social Security number to open an account, and you need a device running Apple iOS 11.0+ or Android 6.0+ (Marshmallow) to use the app.

Say you need a cashier’s check in a pinch to put down a deposit on an apartment. You won’t be able to drive to your local branch to get one.

Instead, you’ll have to contact Simple days in advance, or transfer money out of the account to get the cashier’s check from another bank. If you’re someone who values (or needs) in-person bank services, you may want to look at a local bank or credit union instead.

What types of accounts does Simple offer?

Simple offers five products—online checking, shared checking, high-yield savings, certificates of deposit, and personal loans:

- Online checking: A checking account that comes with a Visa® debit card, mobile check deposit, instant transfers to other Simple users, and external account linking.

- Shared checking: A joint account that you co-own with another person to manage spending and saving. You can invite someone (e.g., your partner or roommate) to open up a shared account through your personal Simple checking account. The shared account will have its own account number and debit cards for both co-owners.

- High-yield savings: Simple’s high-yield savings account is called a protected goals account and has an APY higher than you'll find at traditional banks, and some other online banking companies. You can sign up through an individual or shared checking account.

- Certificates of deposit: The Simple CD earns a fixed APY for a 12-month term. The minimum to open the account is $250 and there’s no penalty for early termination.

- Personal loans: Fixed-rate personal loans are offered to pre-qualified Simple users. Simple doesn’t get into specifics about interest rates, but you can qualify for a 1.00% rate discount if you sign up to make auto-payments from your Simple checking account.

What fees does Simple charge?

Simple bank accounts have no overdraft fees, incoming wire transfer fees, replacement card fees, or ATM fees. Remarkably, the CD doesn't even have an early withdrawal fee. In comparison, major banks and credit unions often charge a portion of the interest earned if you cancel the CD before the term ends.

There are, however, some potential fees to watch out for: A book of checks will run you $5, but you can avoid this if you go completely paperless. You won’t get hit with ATM fees if you withdraw cash within the Allpoint® network, but other operators may charge one. Visa may charge a fee of up to 1% when you use the card internationally.

Since Simple doesn’t charge fees, you may be wondering—where’s the catch? Simple makes money in two ways: Simple gets a cut of the fee that merchants pay when you swipe the card, and it also gets a cut of the interest paid on loans it makes.

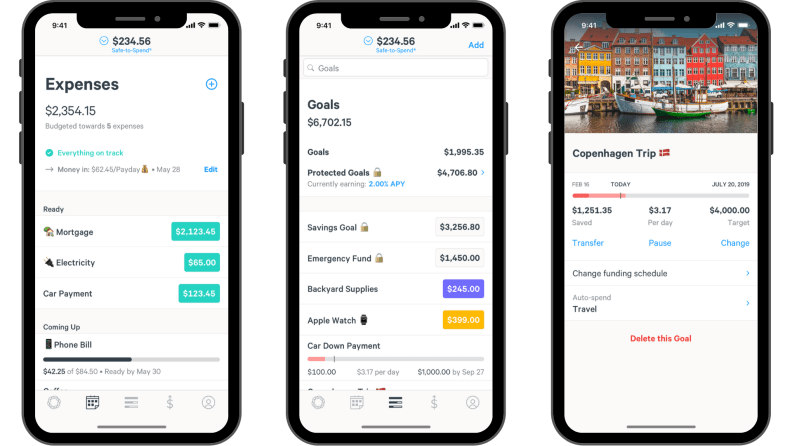

Track your expenses and automate savings goals with Simple's mobile app.

What features are available with the Simple app?

The mobile app has money management tools galore:

- Bill tracking: Input your monthly bills and living expenses into the app and it automatically sets aside money to cover them.

-

Goal setting: After creating savings goals, the app automates allocations to your digital savings envelopes.

- “Safe-to-spend” feature: The app lets you know how much is safe to spend after you manually input your monthly bills and savings goals. You can make smarter on-the-spot decisions, like whether you have enough money for Uber or you’re better off taking the subway.

- Transaction round-ups: This feature rounds up card transactions to the next whole dollar and then transfers the difference into savings once the total reaches $5.

- Card blocking: If you lose your card, you’re able to block and unblock your card within the app.

How can Simple help you manage your money?

Depositing funds into your account is easy enough—you can set up direct deposit, deposit a check through the mobile app, or transfer money from an external account. Keep in mind that Simple does not accept cash deposits through ATMs. According to the website, the quickest way to get cash into your account is by getting a money order and depositing it via mobile check deposit.

You simply enter the due dates for your various bills and living expenses. Then you set an amount and deadline for short- and long-term goals, like putting aside $3,000 for braces or $10,000 for a down payment.

It’s worth noting this budgeting feature is not automatic bill pay; rather, the money is allocated to each expense envelope and you have to remember to use the cash to pay bills.

What security and protection does Simple offer?

Funds in your Simple account are held at BBVA USA, an FDIC-insured bank. FDIC insurance means the money in your account is insured up to $250,000 should the bank fail.

Cardholders are also covered by Visa Zero Liability. Under this protection, you’re not liable for unauthorized credit transactions as long as you notify Simple within two business days. Otherwise, you could be liable for up to $500. As for unauthorized debit transactions, as long as you notify Simple within two business days, you'll only be liable for $50.

Simple goes beyond online checking, with high-yield savings accounts and CDs.

How does Simple stack up to other banks?

When this review was published, Simple offered 1.40% APY on its savings account—at the time, generous considering the national average for savings was just 0.07% APY. For a head-to-head comparison, Ally Bank offered a slightly lower APY, but Simple has since significantly lowered the rate. Chime's current APY comes in higher than both.

When it comes to CDs, however, Simple's APY is not the highest around. Ally Bank, for example, also offers no early termination fees, with greater interest on 11-month CDs. While Barclays does charge for early withdrawal, it does offer a higher APY for its 12-month terms. Plus, Simple requires $250 to open a CD account, whereas, Ally Bank and Barclays do not require a minimum balance.

What drawbacks does Simple have?

The online banking services are somewhat limited. Simple is not a major bank or credit union with a large portfolio of products like credit cards, mortgages, or auto loans that you can apply for and manage under one account. Again, there are no physical locations you can visit to handle banking tasks.

Simple no longer offers online bill pay either, which is a service offered by banks that can automatically send out recurring payments from your account to individuals or companies each month. Simple axed online bill pay in 2019 to the frustration of many users. But what Simple lacks in bells and whistles it makes up for with a lack of fees.

So, should you open a Simple account?

The Simple account lives up its name. If you’re looking for a basic account to store your money with features like expense tracking and downloadable statements to help you manage cash flow, this product is worth considering.

You can manage your household budget and goals in one place while you both maintain individual accounts for your personal money. Chime, one of Simple’s competitors, does not offer joint accounts at the moment.

Simple doesn’t come with all of the extra perks of accounts offered by larger institutions. But if avoiding fees is higher on your priority list than in-person banking, Simple has a lot to offer as far as savings and money management features.

The product experts at Reviewed have all your shopping needs covered. Follow Reviewed on Facebook, Twitter, and Instagram for the latest deals, product reviews, and more.